Senior Property Tax Relief: What It Is and How It Helps Homeowners

When you’re over 65 and living on a fixed income, a rising property tax bill can feel like a punch in the gut. Senior property tax relief, a set of government programs designed to reduce or delay property tax payments for older homeowners. Also known as property tax exemptions for seniors, these programs exist in many U.S. states and are slowly being adopted in parts of India to help elderly residents stay in their homes. This isn’t about getting a free ride—it’s about fairness. People who bought their homes decades ago and never moved out shouldn’t be forced out because taxes doubled while their pension stayed the same.

There are three main ways senior property tax relief works: property tax exemptions, a direct reduction in the taxable value of your home, tax freezes, locking your tax bill at the level it was when you turned 65, and tax deferrals, delaying payment until you sell the home or pass away. Each has different rules. In Texas, for example, you can get a $10,000 homestead exemption on top of the regular one. In Maryland, seniors can freeze their taxes if their income is under $60,000. In India, some cities like Bengaluru and Pune now offer up to 50% reduction for seniors over 60 who own only one home.

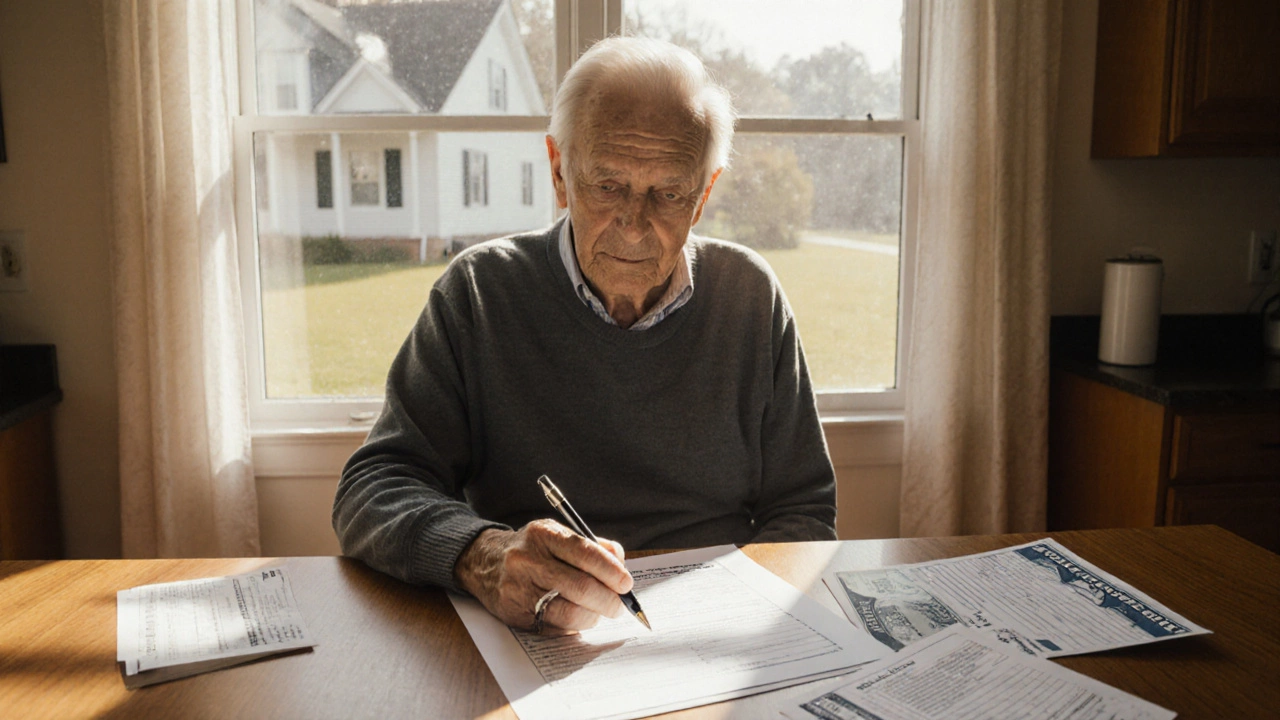

These programs don’t just help with cash flow—they keep communities intact. Grandparents stay near their kids. Longtime residents don’t get pushed out by gentrification. But here’s the catch: you have to apply. No one sends you a check automatically. You need to file paperwork, prove your age, show your income, and sometimes prove you live there full-time. Missing the deadline? You lose the break for the year. And not every county or city offers it. That’s why knowing your local rules matters more than national headlines.

Many seniors don’t realize they qualify because they think it’s only for the poor. But even if you have a pension, Social Security, or a small retirement account, you might still qualify. Some programs look at total household income, not just your salary. Others only care if you own one home. And if you’re a widow or widower, you often get to keep the benefit even if your spouse was the original applicant.

What you’ll find in the posts below aren’t just articles about tax law—they’re real stories from people who used these programs to stay in their homes. You’ll see how someone in Virginia saved $1,200 a year with a freeze. How a retired teacher in Maryland kept her house after her landlord tried to sell. How a senior in Texas used a deferral to afford medical bills. These aren’t theoretical fixes. They’re tools that work—if you know where to look.

Oct, 28 2025-0 Comments